Sir Paul Collier wants to infuse Economics with some Ethics. We would prefer to start with Ethics and build some Economics around it.

The Future of Capitalism (2018) By Sir Paul Collier

- Goodreads Rating: 3.86

- Amazon Rating: 4.4

- 256 Pages

- Kindle: $10.99

- Paperback: $28.38 (Spanish Edition only)

Product details

- Publisher : Harper; 1st Edition (December 4, 2018)

- Language : English

- Hardcover : 256 pages

- ISBN-10 : 0062748653

- ISBN-13 : 978-0062748652

- Item Weight : 15.7 ounces

- Dimensions : 6 x 0.89 x 9 inches

- Best Sellers Rank: #163,890 in Books (See Top 100 in Books)

- #89 in Business Planning & Forecasting (Books)

- #125 in Free Enterprise & Capitalism

- #129 in Income Inequality

- Customer Reviews: 4.4 out of 5 stars 411 ratings

About The Author:

Sir Paul Collier, knighted in 2014 for empowering positive changes in African economic policy, is currently a professor of economics and public policy at Oxford’s Blavatnik School of Government. He is also a Senior Fellow at the Milken Institute, a “nonprofit, nonpartisan think tank” that is trying to utilize current research and bring all relevant voices – no matter how divergent their opinions – into a productive dialog, in order to “construct programs and policy initiatives” that ultimately benefit people’s lives at the community level.

Sir Paul’s research has centered around the issues facing the world’s more “fragile states”; how geography, natural resource management, urbanization, culture, and private investment – aka all things ‘globalization’ – have had a more pronounced negative effect on the developing world, because they have not been afforded the ‘social paternalism’ of established governments, such as those found within the ‘developed world’ (economics likes to call developed countries economically ‘more mature’, but it is only that their governments are more mature – meaning well-established prior to the infusion of a large-scale economic infrastructure).

Sir Paul also serves as the director of the International Growth Centre, and sits on the advisory board of ASAP (Academics Stand Against Poverty); he formerly directed the Development Research Group at the World Bank, and served as senior advisor to the Blair Commission for Africa.

About the Book:

“Belonging is the foundation for reciprocal obligations…The balance between selfishness and reciprocal obligations – between individualism and community – plays out in the new geographic divide, between booming metropolis, and broken provincial cities…[and] the new class divide between the prosperous educated and the dispairing less educated…”

Sir Paul Collier is yet another economist whose research shows that leaving markets to their own “individual self-interest” only increases our financial, geographic, and social divide. The numbers have also shown that after-the-fact “social paternalism” has been equally ineffective. This is because oppression, followed by some form of ‘reparations’, cannot erase the original sin of the oppression, and the psychological damage it generates; there needs to be a third way forward – one that steers us straight down the middle of the road, versus constantly swerving right then left in some drunken political power grab at the economic steering wheel.

As an ‘old school’ economist, Sir Paul still believes Capitalism is the ultimate vehicle to drive us forward, even though it continues to run over the same people, crashes on occasion, pollutes all the time, constantly needs to be refueled, and leaves 99% of us behind (who inexplicably wind up having to pay the bill for all this damage). The optimist in Sir Paul proposes that we infuse Capitalism with some ‘ethics’ – akin to teaching a pig to sing – meanwhile, he hedges this long shot bet with suggestions for more ethical tax and transfer ‘reparations’ that hope to be less offensive to the rich.

His research has uncovered an immense amount of economic ‘rent’ (called ‘agglomeration’) accruing within large booming cities. ‘Rent’ is the ‘money for nothing’ that goes straight into wealthier landlord’s pockets, who reap the rewards for owning resources (like housing) that are allowed to rise because of the ‘demand’ for it. ‘Demand’ is Capitalist-speak for legalized profiteering, which occurs most rampantly in areas like housing, health care, and other essential human needs that have yet to be recognized as ‘human rights’ – not that declaring them as such holds much sway with a Capitalist, anyway.

The people who congregate in a city, in effect, wind up creating their own ‘economies of scale’. From infrastructure to distribution channels, overall costs are lowered, though in the ass-backwards world of Capitalist Economics, economic ‘rent’ still rises, and the people are penalized for what should be a more efficient / effective economic (and public) win / win.

While Sir Paul is hoping to get Capitalism to sit down and have a dialog with Ethics, several other economists have joined him in advocating for a more ‘interdisciplinary’ kind of training, in order to better factor people into the detached math dominating the current economic equation. Sir Paul feels that ‘ethics’ – or infused values – will help create a more inclusive kind of decision-making. “These belief systems can be built consciously by leaders at the hub of networks: in families, firms, and societies.”

Sir Paul clearly realizes that a declaration of various ‘human rights’ has done little to guarantee them, especially among the more fragile nations of the developing world. Through embracing a more communal (or ethical) spirit, the pragmatic logic of “reciprocal obligations” (conferring mutually-desired outcomes upon each other) would likely do more to ensure what ‘human rights’ has too-often failed to deliver. (For example: instead of declaring a right to life that clearly does not exist – even in the United States – we would instead admit to each other that “I don’t want to kill you and you don’t want to be dead”.)

Sir Paul, ever the pragmatist, simply wants the results that any reasonable person would want, however they can be achieved; the only stumbling block is that we must procure them from the most unreasonable group of people ever assembled; the winners in a game where sharing is not only a losing strategy, it is downright treasonous.

Third Option Takeaways:

Sir Paul (like Thomas Paine, Henry George, and more recently, Joseph Stiglitz) believes that there is value that individuals create (good for them) and there is value that society creates together – what one might call ‘shared value’. This ‘shared value’, Sir Paul and others believe, should actually be shared; a radical notion, perhaps, unless a society is truly democratic – then it should be expected.

The land area controlled by a nation-state, along with the resources on or below it, is one such value a truly democratic population might share. Any rent accrued through the creation of money (aka bank ‘interest’) would be another, as money is made sovereign by the ‘consent of the governed’, in order to serve as the lifeblood of that nation’s economy, and the measure of whatever value it creates. Sir Paul has, in essence, found a third shared value: the ‘agglomeration’ of people into one small space, that causes prices to rise independent of any effort on the part of landlords or merchants – this form of rent could also, through taxation, be shared among the members of a community.

The Third Option believes that all value, in some small way, is ‘shared’ value. From creation to consumption, each of us represents a link in this economic chain that must remain unbroken for economics to function properly. To believe that some wealthy individual – investing money they likely inherited – is somehow irreplaceable in this economic sequence smacks more of paternalism than any egalitarian redistribution scheme.

If owning two or three houses or spouses will make someone MORE happy, more power to them, but only up to the point where it interferes with another citizen’s liberty, freedom, happiness or survival; that is where the buck needs to stop.

People – we all know one – can be hard-working, innovative, adaptive, passionate; these qualities exist prior to some Capitalist pulling out their wallet. Capitalism does not prevent idleness. It ‘banks’ on the fact we cannot sit still. Like the resources of the planet, it extracts what already exists to serve its parasitic purpose: to get fat off the lifeblood it sucks from each one of us.

Every human is born with a drive for MORE. When we seek the MORE from within ourselves, this is what makes us Powerful. This inner passion is the true Will to Power. When we seek the MORE from outside ourselves, this is what makes us Controlling. Someday, we will stop mis-labeling the two; then perhaps, we will stop allowing ourselves to be Controlled, and together, begin to harness our collective Power.

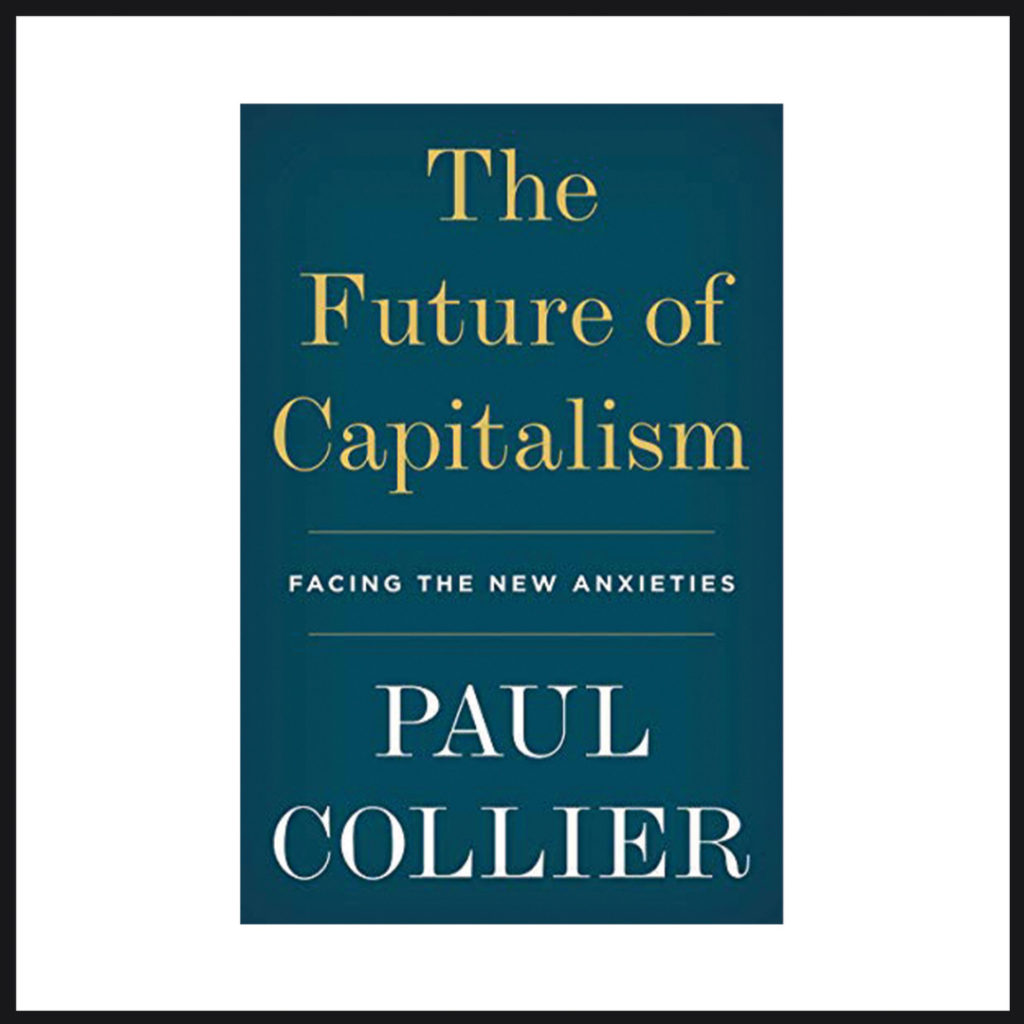

Economic Growth certainly means nothing tangible to 99% of us – but it could. The eco-nomics of the planet (prior to our disruption of it) is a masterpiece of self-sustaining efficiency and effectiveness. It is circular, infinitely recyclable, and fully self-contained. In order to achieve this kind of circular economy, we need to funnel all the ‘value’ we generate in and out of a single source, so that whatever effort each of us puts forward, some small percentage gets collected and redistributed, so we all feel the benefit of this shared ‘Economic Growth’.

In The Third Option plan, the new Economic Growth Collector would be a National Public Bank (perhaps eventually a ‘World Bank’, but first we should ‘beta test’ the idea on ourselves, before we go unleashing any more of our big ideas on the neighbors). The Bank would be funded with a 10% ‘flat’ tax on the gross revenue generated by all citizens – which includes corporations (an Economic Rent Tax – for anything of shared value that is utilized for individual gain – could also be added to the pot). Thus, individuals would retain 90% of what they earn, while the annual value created by all citizens would still be represented within this Bank (the 10% flat tax). To empower assured value creation, the Bank would allocate financing to create all the essential needs infrastructure, dispersed equally among every community, per our ‘reciprocal obligations’ to each other, meanwhile retaining federal government departments for all essential needs, in order to help manage these larger projects at the community level.

Essential Needs:

Healthcare, Education, Employment, Housing, Water / Sewer, Communication, Transportation, Energy, Food (Agriculture), Financial Retirement Security

The loans to each community, that help create this infrastructure, would be paid back through affordable monthly bills for the products and services rendered. The necessary employment of citizens within each community to render these products and services would not only provide them with a steady income, but automatically create the 10% flat tax necessary to fund the next round of investments.

Private ‘investment’ banks would still exist, in order to fund anything not considered an essential need, but the National Public Bank would be the Central Bank, so would lend the money to the private banks, as they would no longer be allowed to create their own money. Because corporations have been declared ‘citizens’, they will face the same IRS tax rules that individual taxpayers face (see gambling income and losses). When projects are slow in any given year, part of the $28.6 trillion National Debt can be syphoned into the Bank in order to pay it back. All loans must be paid back at 4% interest, which will grow annually, and be divided among all citizens when they reach retirement age, as a more sustainable form of social security.

Other Works By Sir Paul Collier

Books:

- Greed is Dead: Politics After Individualism

- The Bottom Billion

- Wars, Guns, and Votes

- Exodus

- The Plundered Planet

- Conflict, Political Accountability, and Aid

Articles:

- “A Path out of the West’s Malaise”

- “Guinea’s Battle Against Corruption: Which Side is the West On?”

- “Why Denying Refugees the Right to Work is a Catastrophic Error”

- “The Rise of Populism: Case Studies, Determinants and Policy Implications”

Interviews:

- “An Interview with Paul Collier”

- “How to Fix Democracy”

- “The Fate of Capitalism Lies in the Hands of the Young”

- “Prolonged Lockdowns are a Route to Poverty”

- “Divisive and Decisive Times”

- “Rethinking Roles and Responsibilities for Africa’s Economic Recovery”

- “On African Recovery”

Videos:

- “Helping Africa’s Firms Survive the Pandemic”

- “The Future of Capitalism”

- “On Capitalism, Education, and Populism”

- “The Future of Capitalism”

- “How to Fix Democracy, Season 2”

- “In conversation with Paul Collier”

- “The Bottom Billion”

Social Media:

Twitter: @BlavatnikSchool and @OUPEconomics

Saving Capitalism: For the Many, Not the Few by Robert Reich – a Book Review

Saving Capitalism: For the Many, Not the Few by Robert Reich – a Book Review